Bullets:

Australia hopes to build supply chains for rare earth metals that are not reliant on China.

In addition to the mining of the metals, they seek to create new industries for separation and refining, to capture significantly more value-added profits downstream of the mining.

But Australia would still be dependent on China for reagents, and for shipping to final users--the manufacturers of magnets. And those end users are all in China.

Australian industry would also struggle to compete against China's lower costs. Specialized labor, logistics, materials, capital expenses, and electricity all are several times more expensive in Australia, compared to China.

What's more, for many rare earth metals, today’s wholesale pricing is far above companies' cost of production. Only a handful of companies are making money industry-wide, and this is a high hurdle in attracting non-Chinese investors into new mining projects.

Report:

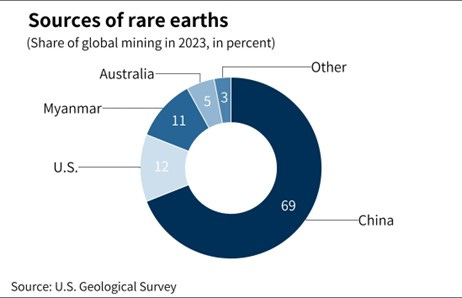

Good morning. This story is emblematic of so many in mining and supply chains, and puts a spotlight on a lot of the issues here. Australia wants to build supply chains for rare earth metals that are independent of China. And that’s proving hard to do. Victoria has heavy mineral sands that are rich in the rare earth metals used to make magnets. The problem is that China makes most of those magnets. They’re the end user.

Chinese companies are typically the lead investors of projects as well. Shenghe Resources is developing two heavy mineral sands projects in Victoria, and has signed contracts that guarantee 60% of the mining output in one project with VHM, and is a 9.9% shareholder in the second one.

The head of VHM said that Shenghe’s capital and expertise were necessary to make the project go. Shenghe will be the offtake of the raw sands, the ores, and the refining will happen in China.

Australia wants to develop its own rare earth refining industry, which is downstream of the mining itself. There are two steps to that process—separating and refining. Refining is where a lot of the value-added is, and most of that is in China. And experts say that even if Australia can do the separation of rare earths, they still will need to go to China for refining. “It’s funny how everything ends up in China anyway”—says this industry insider, and it’s because that’s where the end users are.

And it’s ultimately a cost problem. Separating rare earths outside China would be many times more expensive, and separators would still depend on China for reagents, then shipping to China anyhow for the rest of it.

What makes the costs so much higher are just what we would think—high labor costs, high materials costs, and high energy costs. Lynas is a Japanese-backed company in Australia, and Lynas has postponed plans to further develop a new plant in Western Australia because of the power problem. They opened a factory for cracking and leaching, but anything beyond that is dependent on more affordable and more reliable energy. Australia’s plan is called the “Future Made in Australia” policy, and that’s not going anywhere unless they can solve the energy problem.

Here’s a map you’ve seen before, for electricity prices from around the world. The darker the color, the higher the prices. Australia and Japan have the most expensive electricity in this half of the world, so they are the very least likely places to put an industry that demands a lot of power. China’s energy costs are a third of Australia’s.

High labor costs and transport costs factor in, too, and Lynas is seeing their profit margins squeezed on the other side by falling prices. Some rare earth metals prices are down sharply, year-over-year. Let’s make a distinction here, between the rare earths that Australia is producing here in their Heavy Minerals Sands, and gallium and germanium and other rare earths that China has put export bans on. Prices on those are rocketing higher. But for neodymium and dysprosium, they’re both down over 20% on the year, and the price index of about a dozen rare earths show the same 20% drop.

So there are mines around the world that can’t break even at these price points. Lynas’s profits are way down but still positive, and China Northern Rare Earth Group is also still making money. But with prices going down, and labor and energy costs high, it’s impossible to attract new investors who aren’t Chinese companies. Nobody else can make money.

Resources and links:

Nikkei, In mineral sands, Australian rare earth ambitions mingle with China's interests

Lynas CEO: Cheap power 'fundamental' to Australia's industrial hopes

No longer rare: China's overproduction sends rare-earth prices tanking

Cost of Electricity by Country 2024

https://worldpopulationreview.com/country-rankings/cost-of-electricity-by-country

Australia's Lynas nears start of heavy rare-earth processing amid China shift

https://asia.nikkei.com/Business/Markets/Commodities/Australia-s-Lynas-nears-start-of-heavy-rare-earth-processing-amid-China-shift

Lots of good points there. Australia has had governments that have off shored manufacturing via various polices since Gough Whitlam and GATT agreements. The last industry to be dismantled was the passenger vehicle with closure of GM and Ford some years ago. Now that the Atlantacist version of globalism is in severe decline Australia is caught between it's commitment to US leadership and alliances, and its on again, off again dance with China. Based on past performance Australia's place in the world will be determined by what Washington permits.